What is High Frequency Trading?

High frequency trading (HFT) implements complex algorithms that can execute thousands of trades in milliseconds often capturing microscopic gains on bid/ask spreads. HFT programs have the advantage of virtually unlimited capital, latency and market access. Proponents of HFT claim these programs provide liquidity in the markets. However, many argue the effect is opposite as HFT programs actually front run trades, which ultimately cost the trader more money. Detractors claim HFT programs are skimming profits from extorting liquidity and are responsible for unnecessary volatility in the markets.

The Scale of High Frequency Trading Programs

Electronic market making is one of the heaviest uses of HFT programs. High frequency trading and algorithm program trading generate up to 70% of total trading volume for U.S. equities markets. HFT programs have expanded worldwide to literally every financial market. In South Korea, HFT accounts for 40% of all trading volume. Firms and hedge funds are in a race to find any niche with HFTS. Machine learning is the next frontier as algorithms get programmed to search for key words through social blogs like Twitter and Facebook to react instantaneously on news and rumors.

What is an Algorithm?

An algorithm is just a fancy name for a computer program that executes a series of instructions under specific conditions. Algorithms process and calculate data to derive and execute problem-solving solutions. Financial firms are heavily utilizing the work of quantitative engineers to devise dynamic pricing models for improved algorithms to exploit a tiny edge in the markets. Algorithms have the ability to repeat processes an infinite number of times to generate large profits from miniscule price discrepancies.

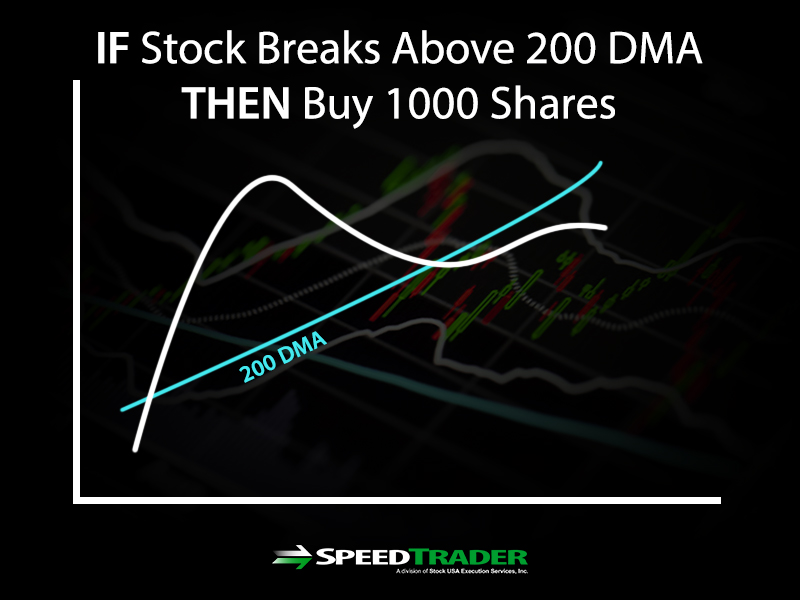

Basic Algorithm

Algorithm programming is getting easier by the day as many standalone products attempt to become more and more user friendly. Algorithms can be as simple as programming a few variables with existing pre-programmed indictors. A simple indicator based algorithm could be programmed as:

If stochastic for XYZ crosses up through the 20-band stochastic on a 5-minute chart, then BUY 100 Shares of XYZ. Sell XYZ position when stochastic reaches 75-band or if stochastic falls under 18-band.

The beauty of algorithms is the infinite number of conditions that can be added onto the existing set of steps. Additional conditions can be added:

Buy XYZ only if share prices are also above the 5-minute 20-period VWAP moving average. Sell XYZ position if price falls below the 5-minute 20-period VWAP moving average.

Professionals and institutions incorporate algorithms with millions of lines of code and conditions.

Key Difference From Retail Traders

While retail traders have access to algorithm programs, there is a vast difference between the complexity and sheer lopsided advantage of a professional high frequency trading program versus a retail algorithm program.

Speed

A high frequency trading programs can execute a trade in less than one millisecond. It takes 300 to 400 milliseconds to blink an eye. Whereas a retail trader that gets a 1 second fill may assume that is fast. An HFT program would have executed 1,000 trades in the same time.

Unlimited Capital

HFT programs are not only backed by millions of dollars in firm capital, but that amount can be leveraged many fold for licensed market makers. Since the positions are usually held for split seconds the buying power is virtually unlimited. The average program trading position holding time is 11 seconds in the U.S. equity markets.

Access to Markets and Pricing

Access to every dark pool and split penny pricing is the distinct advantage. While a retail trader can only place orders with two decimal pricing (eg: $17.22), HFTs can access pricing up to four decimals (eg: $17.2224). It is this microscopic difference that HFTs exploit thousands of time that generate massive profits. When a trader places an order to BUY 1000 Shares of XYZ at $17.24, an HFT can buy at $17.2390 and sell to the trader at 17.2400 to pocket a $0.0010 profit almost risk-free. Rinse and repeat that thousands of times a day and that is how profits grow. Additionally, HFT firms pay large fees to exchanges to access quotes quicker than retail. Fees can range around $300,000 for this privilege for quicker access.

These three advantages give HFT programs a major edge over retail traders. Algorithms have the ability to infinitely repeat instructions without carrying the weight of emotions in the decision making process. However, the growth of HFT and algorithms has spurred furious competition resulting in a leapfrog effect that can magnify price movements drastically in short periods of time. This is where the retail trader can sport an edge. As they say, my enemy’s enemy is my friend.

How HFT Affects Traders

Rampant HFT activity can distort quote pricing making it very tough for traders to get decent fills. In fact, the heyday of HFT was during 2010-2011 flash crash and S&P ratings downgrade of the United States.

Spoofing

In 2012, a mysterious HFT program was released into the U.S. equities markets that single handedly generated 4% of the U.S. stock market quote activity consuming 10% of the total U.S. markets bandwidth, without executing a single trade. Spoofing is considered market manipulation, as the intent is to artificially move prices with no intent to execute. This involves posting large bid sizes in an attempt to spur artificial demand and trigger buyers while sellers lift their asks higher.

The purpose of spoofing is to create an artificial appearance of demand to spur buying or supply to spur selling. For example, if there are 11 bidders of XYZ stock at 17.22 each showing 10,000 shares versus a single ask at 17.24 with 200 shares, then this will panic short-sellers to consider covering while buyers would come off the fence. However, when someone tries to sell 1,000 shares at 17.22, the bids would mysteriously disappear. This leaves the trader with little to no liquidity, unless the spoofer succeeds to luring other real bidders into the market.

It is a game of bluff. However, the latency of HFT programs allow the bluff to rarely ever be called as orders gets cancelled at the slightest threat of being executed. In 2012, a mysterious algorithm program was spoofing hundreds of thousands of spread quotes, which affected price movement, without executing a single trade. Rampant spoofing caused quotes to be delayed. This provides a major edge to HFT programs that can exploit price discrepancies.

Volatility

With so many algorithms active in the markets, this can pose many opportunities for traders especially during the first hour of trading. When algorithms compete against each other, the result can be magnified price movements in short periods of time. For prudent trader, this can mean a day’s worth of profits being attained in minutes. Naturally, the flip-side is that losses can also mount much quicker is the trader is caught on the wrong side. Electronic markets are seeing more and more short-squeezes because of this. One trader’s short squeeze forced liquidation is another trader’s home-run.

Liquidity

High frequency trading programs by design can front-run orders by sniffing out large orders and using the speed advantage to quickly skim thin profits. When multiple HFT programs compete with each other, it results in retail traders having to pay up or chase liquidity. This can be a boon for traders that are already in a position, but a bane for traders trying to get a decent fill. While markets move on thin liquidity, the problem is getting filled without chasing. It can be difficult to unload a 5,000-share position without making a market impact. Therefore, positions often times need to be broken up into smaller sizes to ensure better liquidity. When algorithms sniff a large seller, they will often play keep away, thereby forcing the trader to chase a fill.